Anomaly Detection using Python

In this example we will be using a dataset which contains details of the closing prices for S&P 500 index from 1986 to 2018.

We are going to create a Long Short-Term Memory Network (LSTM) Model.

Step 1: Import Libraries

1import numpy as np

2import tensorflow as tf

3from tensorflow import keras

4import pandas as pd

5import seaborn as sns

6from pylab import rcParams

7import matplotlib.pyplot as plt

8from matplotlib import rc

9from pandas.plotting import register_matplotlib_converters

10from sklearn.model_selection import train_test_split

11from sklearn.preprocessing import StandardScaler

12rcParams['figure.figsize'] = 22, 10

13

14RANDOM_SEED = 42

15np.random.seed(RANDOM_SEED)

16tf.random.set_seed(RANDOM_SEED)Step 2: Upload the Dataset

In this example we will be using a dataset that can be downloaded from Kaggle.

1anomaly_df = pd.read_csv('/content/spx.csv', parse_dates=['date'], index_col='date')Step 3: Manual Anomaly Detection

1fig = plt.figure()

2plt.style.use('ggplot')

3

4ax = fig.add_subplot()

5

6ax.plot(anomaly_df, label='Close Price')

7

8ax.set_title('S&P 500 Daily Prices 1986 - 2018', fontweight = 'bold')

9

10ax.set_xlabel('Year')

11ax.set_ylabel('Dollars ($)')

12

13ax.legend()

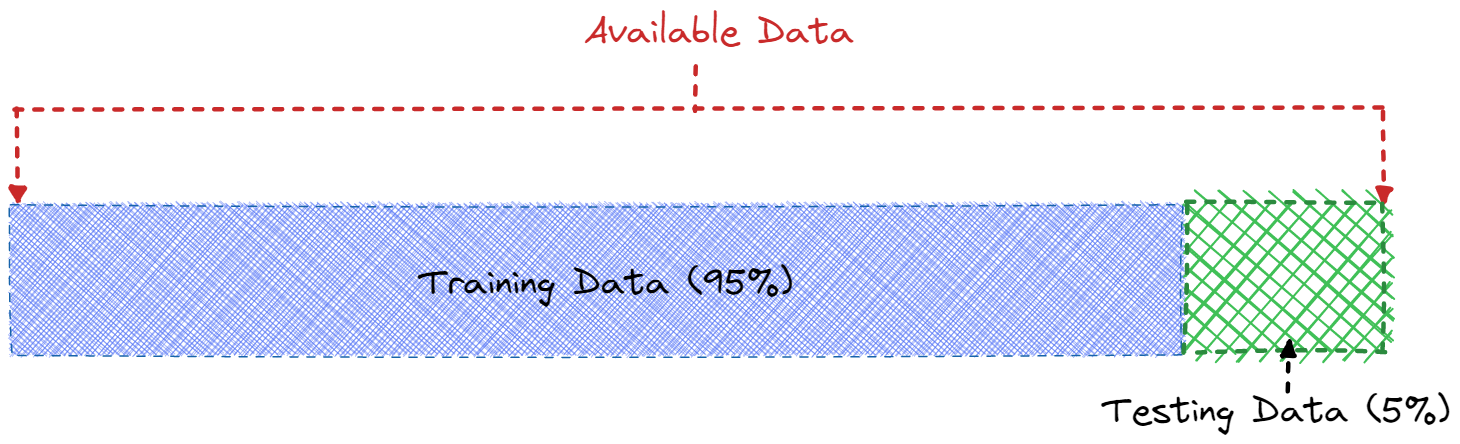

Step 4: Splitting the Dataset into Training & Testing

In this example, we are choosing to split the data into two parts:

- 95% training data, to train our machine to learn the normal patterns in the data

- 5% testing data, to evaluate the machine.

1train_size = int(len(anomaly_df) * 0.95)

2test_size = len(anomaly_df) - train_size

3train, test = anomaly_df.iloc[0:train_size], anomaly_df.iloc[train_size:len(anomaly_df)]Step 5: Preparing the Data

First we will scale and reshape our data for the ML model.

1scaler = StandardScaler()

2scaler = scaler.fit(train[['close']])

3

4train['close'] = scaler.transform(train[['close']])

5test['close'] = scaler.transform(test[['close']])1#Create helper function

2def create_dataset(X, y, time_steps=1):

3 Xs, ys = [], []

4 for i in range(len(X) - time_steps):

5 v = X.iloc[i:(i + time_steps)].values

6 Xs.append(v)

7 ys.append(y.iloc[i + time_steps])

8 return np.array(Xs), np.array(ys)

9

10TIME_STEPS = 30

11

12# reshape to [samples, time_steps, n_features]

13

14X_train, y_train = create_dataset(train[['close']], train.close, TIME_STEPS)

15X_test, y_test = create_dataset(test[['close']], test.close, TIME_STEPS)Step 6: Create the Model

1model = keras.Sequential()

2

3#encoder

4model.add(keras.layers.LSTM(

5 units=64,

6 input_shape=(X_train.shape[1], X_train.shape[2])

7))

8model.add(keras.layers.Dropout(rate=0.2))

9

10#decoder

11model.add(keras.layers.RepeatVector(n=X_train.shape[1]))

12

13model.add(keras.layers.LSTM(units=64, return_sequences=True))

14model.add(keras.layers.Dropout(rate=0.2))

15

16model.add(keras.layers.TimeDistributed(keras.layers.Dense(units=X_train.shape[2])))

17

18model.compile(loss='mae', optimizer='adam')

19model.summary()Step 7: Train the Model

To create our model we need to decide on the most appropriate batch size and number of Epochs, changing these values will vary our models performance.

1history = model.fit(

2 X_train, y_train,

3 epochs=10,

4 batch_size=32,

5 validation_split=0.1,

6 shuffle=False

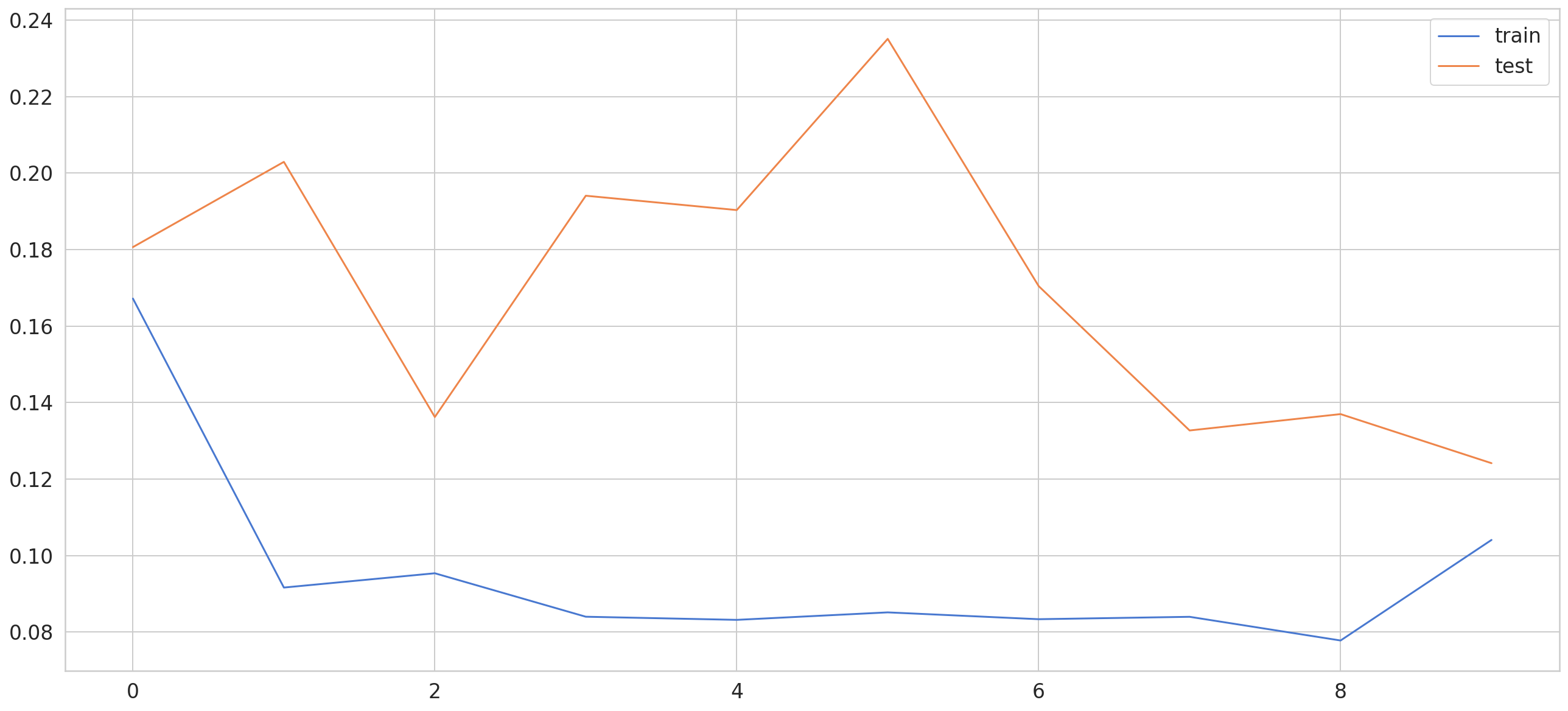

7)To decide what is the suitable number of epochs we can visualize the result from our model.

1fig = plt.figure()

2ax = fig.add_subplot()

3

4ax.plot(history.history['loss'], label='train')

5ax.plot(history.history['val_loss'], label='test')

6

7ax.legend()

Step 8: Defining the Anomaly Value

First we will calculate the loss between the predicted and the actual closing price data:

1X_train_pred = model.predict(X_train)

2

3train_mae_loss = np.mean(np.abs(X_train_pred - X_train), axis=1)We will then plot the loss distribution to decide on the threshold for our anomaly detection.

1fig = plt.figure(figsize=(20,10))

2sns.set(style="darkgrid")

3

4ax = fig.add_subplot()

5

6sns.distplot(train_mae_loss, bins=50, kde=True)

7

8ax.set_title('Loss Distribution Training Set ', fontweight ='bold')

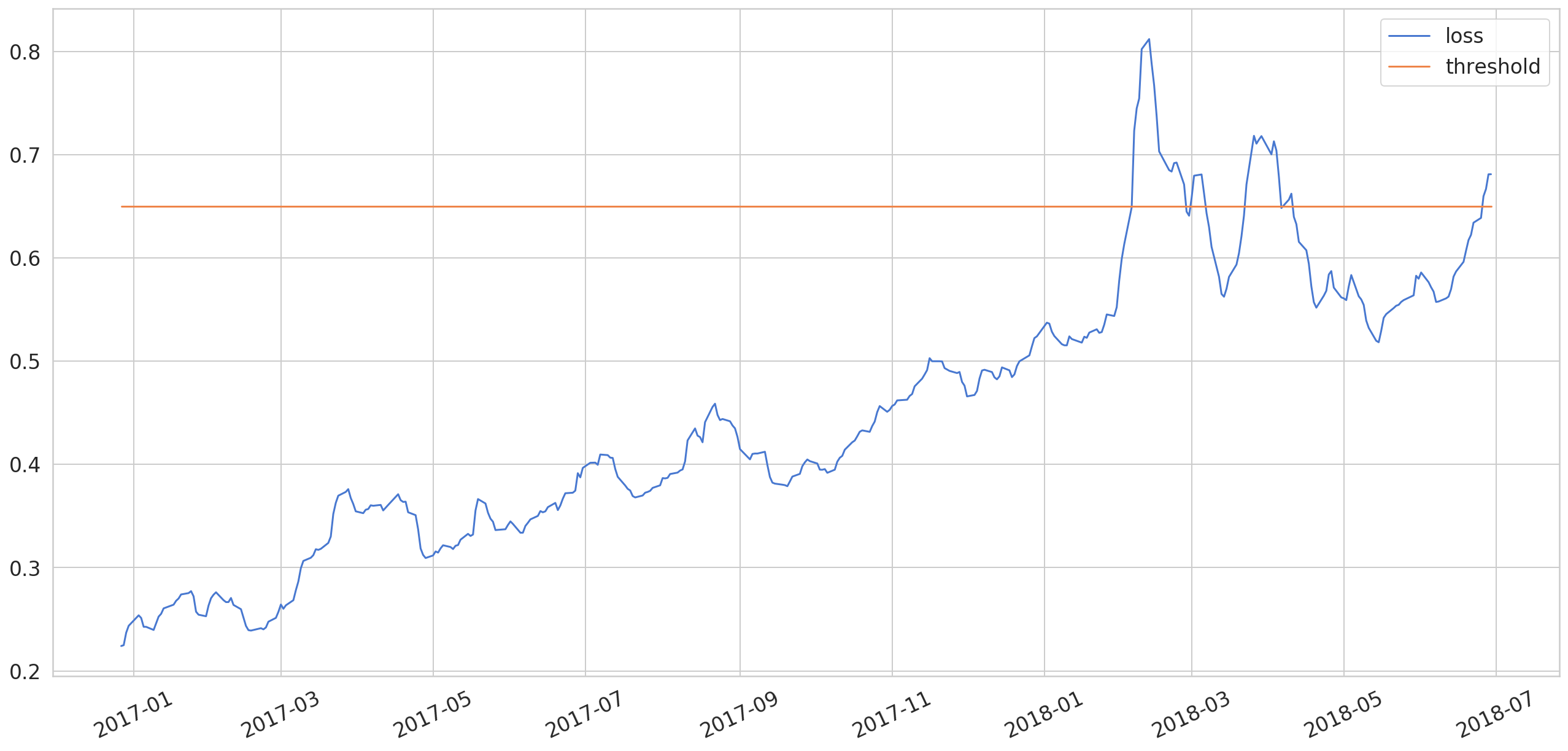

Calculate the Mean Absolute Error

1X_test_pred = model.predict(X_test)

2

3test_mae_loss = np.mean(np.abs(X_test_pred - X_test), axis=1)In this example we are using a threshold of 0.65

1THRESHOLD = 0.65

2

3test_score_df = pd.DataFrame(index=test[TIME_STEPS:].index)

4test_score_df['loss'] = test_mae_loss

5test_score_df['threshold'] = THRESHOLD

6test_score_df['anomaly'] = test_score_df.loss > test_score_df.threshold

7test_score_df['close'] = test[TIME_STEPS:].close1fig = plt.figure()

2

3ax = fig.add_subplot()

4

5ax.plot(test_score_df.index, test_score_df.loss, label='loss')

6ax.plot(test_score_df.index, test_score_df.threshold, label='threshold')

7

8ax.legend()

1anomalies = test_score_df[test_score_df.anomaly == True]

2anomalies.head()And finally our anomaly detection.

1fig = plt.figure()

2

3ax = fig.add_subplot()

4

5ax.plot(test[TIME_STEPS:].index,

6 scaler.inverse_transform(test[TIME_STEPS:].close.values.reshape(1,-1)).reshape(-1),

7 label='close price')

8

9sns.scatterplot(anomalies.index, scaler.inverse_transform(anomalies.close.values.reshape(1,-1)).reshape(-1), color=sns.color_palette()[3],

10 s=52,label='anomaly')

11

12ax.legend()

We can change our anomaly threshold which will enable our model to detect more or less anomalies depending on your businesses criteria.